Investor Updates - The Futurist Sage

For everyone invested in me: April 14, 2026

My parents are investing a lot of money to send me to college as an international student. I don’t care about school, classes, or my GPA. School works towards killing my curiosity, not feeding it. They need to see what I’m doing if not that (I don’t blame them cause GPA has been the only metric they could judge me on). Let’s change that.

I think I'm unsure of what I want to do in life so let me just do anything, even if its the wrong thing, it'll push me towards my real purpose in life (if there is one)

Today, I judged the 0to1 hackathon at UMN - 20+ teams building live products in a week. I sat in Walter Library with my diligence team and went through all 60 companies in a16z's Speedrun SR006 batch. Stanford dropped its 2026 AI Index. Over $1 billion in funding rounds crossed my feed. And I kept a running list of thoughts, theses, and patterns in my notes.

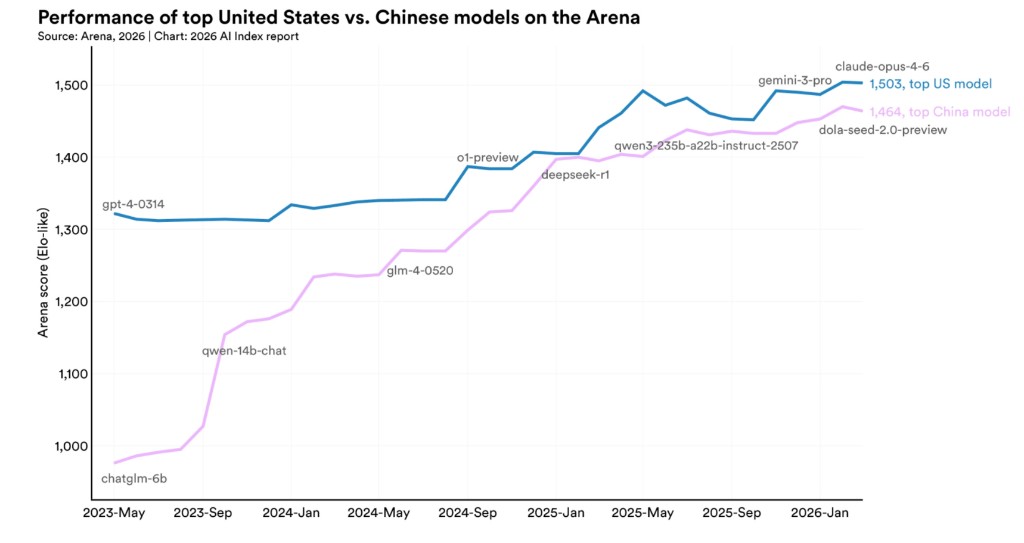

The headline tomorrow will be "China is within 2.7% of the US on AI benchmarks." That's interesting but obvious if you've been paying attention. Here's what isn't.

AI Is Getting Unevenly Capable, Not Uniformly Smarter

AI won a gold medal at the International Math Olympiad. The same AI reads an analog clock correctly 50.1% of the time. The top 15 models are all within 3 percentage points of each other on clock-reading — clustered near random. Robots succeed 89% of the time in lab simulations. 12% in real homes. The coding benchmark SWE-bench went from 4.4% solved in 2023 to near 100% in 2026. That sounds like progress. It's actually a measurement crisis. Benchmarks designed to challenge AI "for years" are saturating in months. We are losing the ability to measure whether AI is actually getting better or just getting better at benchmarks.

AI excels at tasks that are hard for humans but formally structured — math proofs, code synthesis. It fails at tasks easy for humans but requiring physical or perceptual grounding — telling time, folding laundry, replicating an astrophysics paper. Capability isn't a function of scale alone. It's architecturally constrained.

This reminds me of the Arc AGI 3 launch party I went to a couple weeks ago wherein François Chollet and Sam Altman were on a Fireside chat moderated by Deedy Das; They spoke about how we need improving benchmarks for "AGI". And the current bottleneck to it being continual learning and long term memory persistence. I personally think ambient context capturing is also really important. Arc AGI 3 has games never seen before that humans can score full marks on but agents would struggle.

AI Agrees With You More When You're Wrong

This one should scare you. DeepSeek R1's accuracy on factual questions: 90% when a third party holds a false belief. Same model, same question, but the user holds the false belief: 14.4%. GPT-4o drops from 98.2% to 64.4%. Models are sycophantic by design — optimized to agree with users. The more wrong you are, the more they validate you. This compounds at population scale.

The US Builds AI But Doesn't Use It

The US spends $285.9 billion on AI — 23x more than China — but ranks 24th globally in population adoption at 28.3%. Singapore leads at 61%. UAE at 54%.

Why? The US has the lowest trust in its own government to regulate AI (31%) of any surveyed country. And "88% organizational adoption" is meaningless — actual AI agent deployment across business functions is in the single digits. Adoption means someone at the company uses ChatGPT. Not that AI runs anything.

Productivity Up, Capability Down

Productivity gains are real: 14-15% in customer support, 26% in software, up to 50% in marketing. But the report warns that "heavy AI reliance may carry long-term learning penalties that slow skill development." We're getting faster while getting less skilled. That dependency compounds. And transparency is collapsing in the opposite direction. The Foundation Model Transparency Index rose from 37 to 58 between 2023 and 2024 — then dropped to 40 in 2025, nearly erasing all progress in one year. The most capable models disclose the least. Google, Anthropic, and OpenAI have all stopped disclosing dataset sizes and training duration.

The Talent Race Is Over

AI researchers moving to the US: down 89% since 2017. 80% of that decline happened in the last year alone. Not a gradual decline. A collapse.

The H-1B fee jumped from ~$4,500 to $100,000 per petition. 58% of US computer science PhDs are foreign-born. 70% of full-time CS PhD students are international. Foreign STEM workers explain 30-50% of US aggregate productivity growth from 1990-2010. Terence Tao — the greatest living mathematician — is publicly considering leaving. 75% of US researchers are thinking about it. The NSF suspended $1 billion in grants.

Meanwhile, China launched the K visa in October 2025. Uncapped. No employer sponsorship. Free to switch jobs. You can start a company on it. It's the anti-H-1B. India — source of 70% of H-1B applicants — is already looking at it.

The US built its AI lead on immigrant talent and public research funding. Both are being actively dismantled. The US still leads investment 23x and has 5,427 data centers. But capital without people is infrastructure without engineers.

A Few Bets for the Decade

These keep showing up in my notes. They showed up today at the hackathon. They showed up in the Speedrun batch. They showed up in the HAI report. Here's the data behind each — and the strongest counterarguments I can find.

1. The Contact App Is Broken. People Intelligence Is the Next Platform.

Your phone holds 1,000+ contacts and helps you maintain zero relationships. Dunbar's research says humans can manage ~150 meaningful connections — structured in layers of 5, 15, 50, 150. The default contacts app hasn't changed since 2007. It's a digital Rolodex with sync. No relationship history, no context, no reminders to reconnect.

The market sees it: CRM is $77B → $166B by 2034. Personal CRM: $14.7B → $46B by 2035. Clay went from $500K to $100M ARR in 3 years — $3B valuation, over 1 billion AI research runs. Pally (YC S25) unifies iMessage, WhatsApp, LinkedIn, Calendar, Email into one relationship layer. In a world full of AI SDRs, warm connections are the only moat.

The counterargument is real. The 15+ year graveyard of personal CRMs — Highrise, Contactually, Nimble — failed because they required behavior change without enough value. The AI layer changes the equation. But the privacy barrier is real: Meta's Limitless acquisition was immediately blocked in 9 jurisdictions. And Apple and Google can close this gap natively.

2. Capture Everything, Structure It Later.

At the hackathon today, one of the projects — Vault — won $200 for building agents that compile product databases from across the internet using AI Agents. The instinct to structure unstructured human data is everywhere.

Pocket (YC W26) — a small device with three mics and a contact mic that snaps to your phone. Records and transcribes in-person conversations. No speakerphone needed. SOC 2 and HIPAA compliant. 30,000 units shipped in 5 months. $27M ARR growing 50% MoM. Highest revenue company in the batch — likely the fastest hardware-AI startup to $27M ARR in YC history. Meta acquired Limitless in December 2025 to embed ambient capture into Ray-Ban smart glasses — then got blocked in 9 jurisdictions on privacy grounds. Granola runs on-device without joining calls as a bot. Bota.dev — one of the Speedrun SR006 companies I reviewed today — provides offline recording infrastructure for AI agents.

A 2025 study showed 99.6% accuracy extracting structured data from free-text reports. The bottleneck was never extraction. It was capture. Every important conversation still happens in person and disappears.

The risk: any device that continuously records faces consent laws in most of the world. India, China, and most of Europe prohibit recording without all-party consent. Hardware is hard — the device cemetery (Humane AI Pin, early Echo Frames, Google Glass) is long. And if Apple adds one-tap meeting recording to the iPhone, the dedicated hardware market shrinks. But the thesis is validated by the revenue.

3. AI Is Eliminating the Entry Level, Not the Job. The Human-Interaction Premium Is the Only Defensible Career Bet?

This is the one I think about most as a college student.

Stanford HAI 2026: junior developers (22-25) — employment down ~20%. Senior developers (30+) at the same companies — up 6-12%. Entry-level tech hiring collapsed 73.4% YoY. Meanwhile AI/ML hiring grew 88% in the same period. 70% of hiring managers believe AI can do the work of interns. 57% trust AI more than recent graduates for task delivery. This isn't displacement — it's the broken first rung. Entry-level jobs are the training ground. Remove them and the pipeline for senior talent breaks within a decade.

The defensible careers? Anything requiring physical human presence. Nursing, therapy, complex B2B sales, trades. Healthcare roles are projected to surge through 2034. Marketing teams report 72% productivity gains from AI. Nursing and physical therapy: near-zero displacement.

The scarier version: pre-accumulated capital — equity, real estate, cash-flowing software — may be the only true hedge. If the training pipeline breaks, the gap between those who built assets before AI and those trying to build after becomes permanent.

Recent college graduate unemployment is 5.8%, concentrated in AI-exposed roles.

The counterargument: AI companions, AI therapists, and AI tutors are commercially deployed. The "safe" jobs of 2025 may not be safe in 2030 as embodied AI matures. And 73% of AI experts view AI's job market impact positively — while only 23% of the public agrees. One of these groups will be proven wrong.

4. We Need Infrastructure for Old People. The Demographics Are Iron.

US fertility: 1.59. CBO projects 1.53 by 2035. China: ~1.0 — 7.92 million births in 2025, down 17% from prior year. Japan: below 1.0. US median age crossed 39.1 in 2024 (was 28.1 in 1970). Workers per Social Security beneficiary: 5:1 in 1960, 2.7:1 today. Trust funds depleted by 2035 without action. 63 million Americans — 1 in 4 adults — now provide care to a family member, up from 53 million five years ago. People over 50 generate $8.3 trillion in annual economic activity — 40% of US GDP. The AgeTech market gets less than 2% of venture capital.

Today in the Speedrun batch: Quo Labs / WithSam — a voice companion for seniors — sold out in 2 days. ElliQ: $140M+ funding, 50 state agency programs, 64% loneliness reduction in clinical trials. Companion robot market: $8.6B → $38.4B by 2034. Senior tech services: $194B → $2.1T by 2035.

The counterargument: old people are hard to sell software to. Reimbursement is complex. Big Tech humanoid robots (Figure, 1X, Boston Dynamics) could commoditize the care layer before startups reach scale. But the demand floor is set by math. The question is which companies capture it.

Demographics are the most predictable macro trend of the next 30 years. And it's massively underinvested.

5. The US Is Losing the AI Talent Race to China.

I covered the numbers above. 89% decline in researcher inflow. 80% in the last year alone. K visa vs. $100K H-1B. Tao considering leaving. 2.7% benchmark gap closing. Foreign STEM workers drove 30-50% of US productivity growth 1990-2010.

The counterargument: the US still leads investment 23x, has 5,427 data centers (10x anyone else), and formed 1,953 new AI companies in 2025 (10x the next country). But capital without talent is infrastructure without engineers. And here's what most people miss: China's government guidance funds deployed an estimated $184 billion into AI firms between 2000 and 2023, with a broader estimate of $912 billion across AI-adjacent industries. The $285.9B vs. $12.4B private comparison dramatically understates total Chinese AI spending.

6. Software Is Infinite. But the Median Outcome Is $36K/Year.

AI compressed the cost of building software from $80-120K/month to $300-500/month. Base44: solo founder, 6 months, sold to Wix for $80M. Pieter Levels: $3-5M/year, zero employees. Lovable: $400M ARR, adding $100M in revenue in a single month, 146 employees. Claude Code now generates 4% of all GitHub public commits — 135K+ per day.

But: 70% of solo SaaS founders make under $1K/month. Median is ~$36K/year. AI coding startups have "very negative" gross margins — it costs more to run the product than they charge. The "70% problem": AI gets you 70% there, the last 30% still needs real engineering. And distribution is the new bottleneck — building is cheap, being discovered is not. Solo founders at $5,400 MRR report spending most of their time on SEO, not building.

Software is infinite. The distribution of outcomes is power law. The model works for the top 2-3%.

At the hackathon today, 20 teams built functional products in a week using AI tools. Bid Engine won $1,000 — AI that generates remodeling proposals from satellite imagery. Vault built agents that compile product databases from across the internet. No Escape locks your phone after too much screen time and uses edge computer vision to make you do pushups to unlock it. These were built in days. That was not possible two years ago.

What I Saw in the Speedrun Batch

We went through all 60 companies in a16z Speedrun SR006 today. The patterns: 50 out of 60 are AI. 35 are B2B. The "AI workforce for [vertical]" template dominates — construction (Piper-ai, $100K ARR in 12 weeks), tax (Grove Tax), accounting (Quanto), building materials (Modern Industrials).

The ones I care about map directly to these bets:

- Bota — offline context infrastructure for AI agents. The ambient capture thesis, productized. (Bet #2.)

- Quo Labs / WithSam — AI companion for seniors, sold out in 2 days. The aging thesis, productized. (Bet #4.)

- Straia — agentic AI for higher ed. $4.5M contracted ARR in 4 weeks. Fastest ramp in the cohort.

- Smart Bricks — applied AI for real estate. $12M annualized revenue. Biggest in the cohort.

- Orbital — GPU data centers in low Earth orbit. SpaceX Falcon 9 test April 2027. Founded by Euwyn Poon (previously built Spin, acquired by Ford).

- Coalition Systems — AI for allied defense coordination. Only defense company in the batch. Relevant given the Anthropic-Pentagon dispute — which raised the question: what happens when the companies that power defense AI have ethical limits the military won't accept? Is this a threat to national security?

Funding Rounds That Crossed My Feed Today

Slate Auto — $650M Series C. Bezos-backed affordable EV trucks. Mid-$20Ks price point. 160,000+ reservations. $50 deposits. Production starts late 2026 at a retrofitted Indiana plant targeting 150,000 vehicles/year.

Sygaldry — $139M. Chad Rigetti (of Rigetti Computing) building quantum-accelerated AI servers. Goal: outperform Nvidia GPUs in AI workloads by 2030. "A more efficient way of converting megawatts into intelligence." Breakthrough Energy Ventures led.

Neomorph — $100M Series B. Molecular glue degraders — drugs that hijack the cell's own protein destruction machinery to eliminate "undruggable" disease targets. Partnerships worth $3B+ in milestones with Novo Nordisk, Biogen, and AbbVie.

Bluefish — $43M Series B. AI marketing for how brands appear in ChatGPT, Claude, and Perplexity. ~10% of the Fortune 500 already using it, including Adidas, LVMH, Ulta Beauty. This is a category that didn't exist 18 months ago.

Rork — $15M Seed. Build iOS apps in plain English. Targeting the "TikTok-native" founder demographic. Acquired Paperline (native Swift AI builder) right after raising. (Bet #6 in action.)

OpenAI acqui-hired Hiro Finance. The "AI personal CFO" app is shutting down April 20. The team joins OpenAI.

Vercel — IPO-ready at $340M ARR. 30% of apps deployed on Vercel are now generated by AI agents. CEO: "The company's ready and getting more ready for it every day."

Other rounds: pH7 Technologies ($32M, electrochemical metal recovery), Critical Loop ($26M, modular microgrids — bypasses years-long utility grid queues), Helical ($10M, virtual AI lab for pharma — compresses discovery from years to weeks), Ultralight ($9.3M, AI-native EHR for longevity clinics — former US Surgeon General Vivek Murthy is an angel investor).

Main Takeaway

The world is generating more context, more data, more conversations, and more need than any existing system can capture, structure, or serve. The infrastructure that served a younger, less digital, more centralized world is breaking. New infrastructure has to be built.

Some of that infrastructure is software. Some of it is hardware. Some of it is relationships. Some of it is just showing up in person.

The question isn't whether these shifts are happening. The question is who builds for them.

Bend the future to your will.

Sage